During the last year, significant progress was made on unifying sustainability reporting standards and terminology. After a long time of shifting viewpoints on what materiality means, who it is for and whether the sustainability sector should even use the term materiality, an agreement has begun to form that materiality is ‘double’ and dynamic.

During the last year, significant progress was made on unifying sustainability reporting standards and terminology. After a long time of shifting viewpoints on what materiality means, who it is for and whether the sustainability sector should even use the term materiality, an agreement has begun to form that materiality is ‘double’ and dynamic.

In this blog, Greenstone will discuss the meaning behind the term 'double materiality' and the reasons why companies should consider a double materiality approach in their materiality assessment.

What is ‘double materiality’?

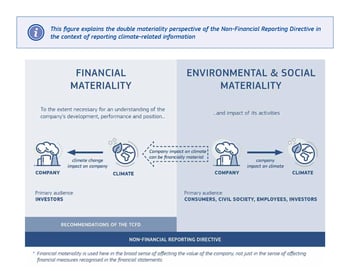

The concept of double materiality acknowledges that a company should report simultaneously on sustainability matters that are:

1) financially material in influencing business value and;

2) material to the market, the environment, and people.

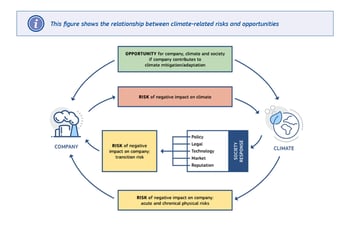

The concept of dynamic materiality acknowledges that the economic materiality of an issue can shift based on anticipated or unexpected circumstances. The concept of “dynamic materiality” was described by the World Economic Forum in a 2020 white paper: “One area in which investors have begun initial explorations is anticipating how issues might become financially material either across an entire industry or for a specific company. What is financially immaterial to a company or industry today can become material tomorrow, a process called ‘dynamic materiality.’”

Source: Overview of the new guidelines on reporting climate-related information (europa.eu)

Why should your company assess double materiality?

Despite having conducted a materiality evaluation, companies might continue to get queries from stakeholders about additional issues. Subjects, such as modern slavery receive Board attention even if they aren't deemed to be material to the business.

The notion of double materiality can be used to respond to stakeholder demands for corporate transparency. Thus, regardless of whether or not they are relevant to the organisation, a company should report on any major external impacts.

At the same time, a company's sustainability team will be able to communicate accurate objectives and push goals that are genuinely a business problem by identifying financially material concerns.

When creating a strategy to manage an effect, such as labour rights in the supply chain, a company needs to determine whether this is a genuine risk for the organisation or whether it is part of the company's obligation to mitigate any impact on people. Double materiality can assist the company in developing an effective management strategy as well as reporting on both internal and external issues to various stakeholders in a relevant manner.

Source: Overview of the new guidelines on reporting climate-related information (europa.eu)

Source: Overview of the new guidelines on reporting climate-related information (europa.eu)

The double-materiality concept: application and issues - a white paper commissioned by GRI, reviews the application of materiality in sustainability reporting – highlighting why disclosing impacts, that go beyond those that are financially material, benefits businesses while supporting sustainable development.

Tips on a successful double materiality assessment

- Strive to get a complete picture of the company’s current and future material concerns. Due to constantly moving factors such as climate change, emerging technologies and new knowledge, companies adapt their products and services and entire industries evolve. Fully understanding the current state of play whilst considering potential future scenarios will allow your material assessments to become more dynamic.

- Familiarise yourself with the various frameworks and standards that have materiality principles (e.g. GRI and SASB) and make the most use of them for the business. The SASB and GRI standards could provide a foundational layer of relevant, comparable, reliable non-financial information across the entire “double materiality” concept.

- Thorough benchmarking will produce a more accurate depiction of business status, allowing you to establish more realistic objectives and build your company's strategy.

- Incorporating current and upcoming policies in your double materiality assessment allows you to stay on top of changes that might have a major impact on the business.

- Once the materiality assessment and matrix are complete, set aside time to monitor and document any changes that influence your material issues.

The scope, timeline, and stakeholder groups engaged in a double materiality evaluation are three key components that differ between definitions. So, keep in mind the idea that materiality at its core is simply disclosing what is important to an organisation.

Further Resources:

- Why double-materiality is crucial for reporting organizational impacts (globalreporting.org)

- SASB Materiality Map

- Greenstone & SASB reporting software